{kind=link}

For most business owners‚ rent‚ staff wages‚ stock procurement‚ utilities‚ and advertising all get evaluated and re-evaluated on a regular basis as they are real costs that affect the business’s bottom line․ However‚ payment processing fees are often overlooked․

Every time a credit card‚ debit card‚ or digital wallet is used to pay for the transaction‚ a percentage goes to the payment processor․ Money is deducted before it gets to your business bank account․

Those automatic and seemingly inconspicuous payments can be a “set it and forget it” expense․ For example‚ these may quietly reduce profits by thousands or tens of thousands of dollars over the course of a month or year․

Understanding payment processing fees is an important first step for businesses seeking to control costs․ A business that regularly analyzes its payment processing fees is often able to find ways to increase cash flow and profit without increasing sales of its products or services․

Table of Contents

Payment Processing Fees Explained

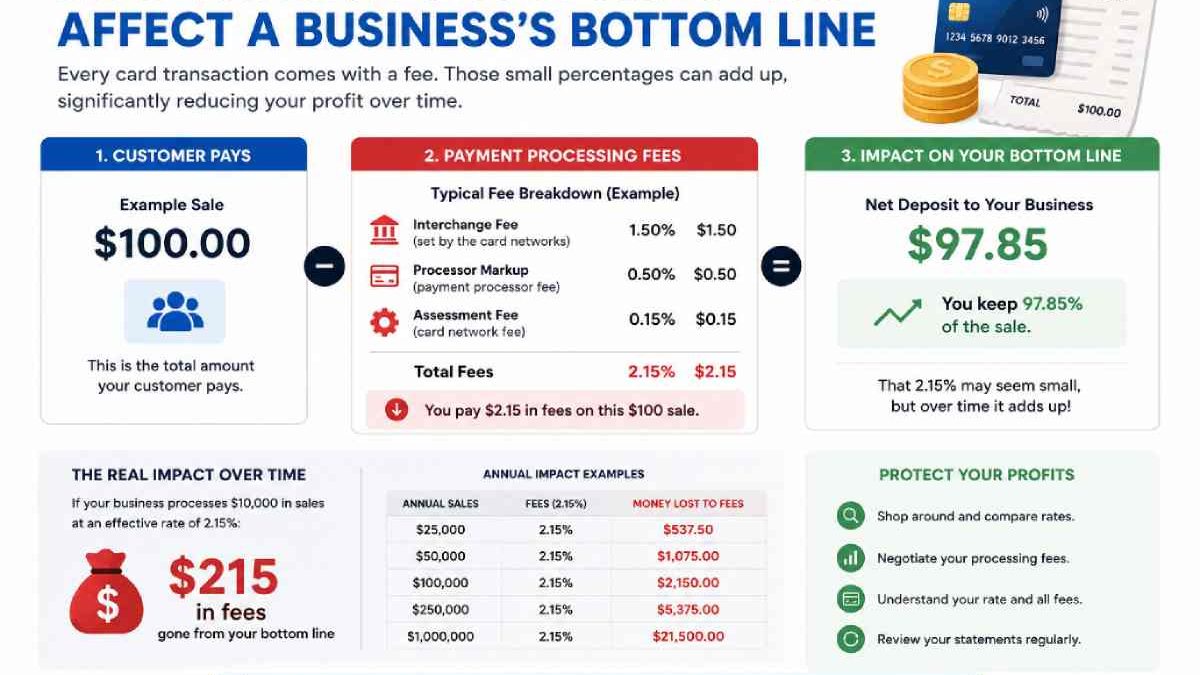

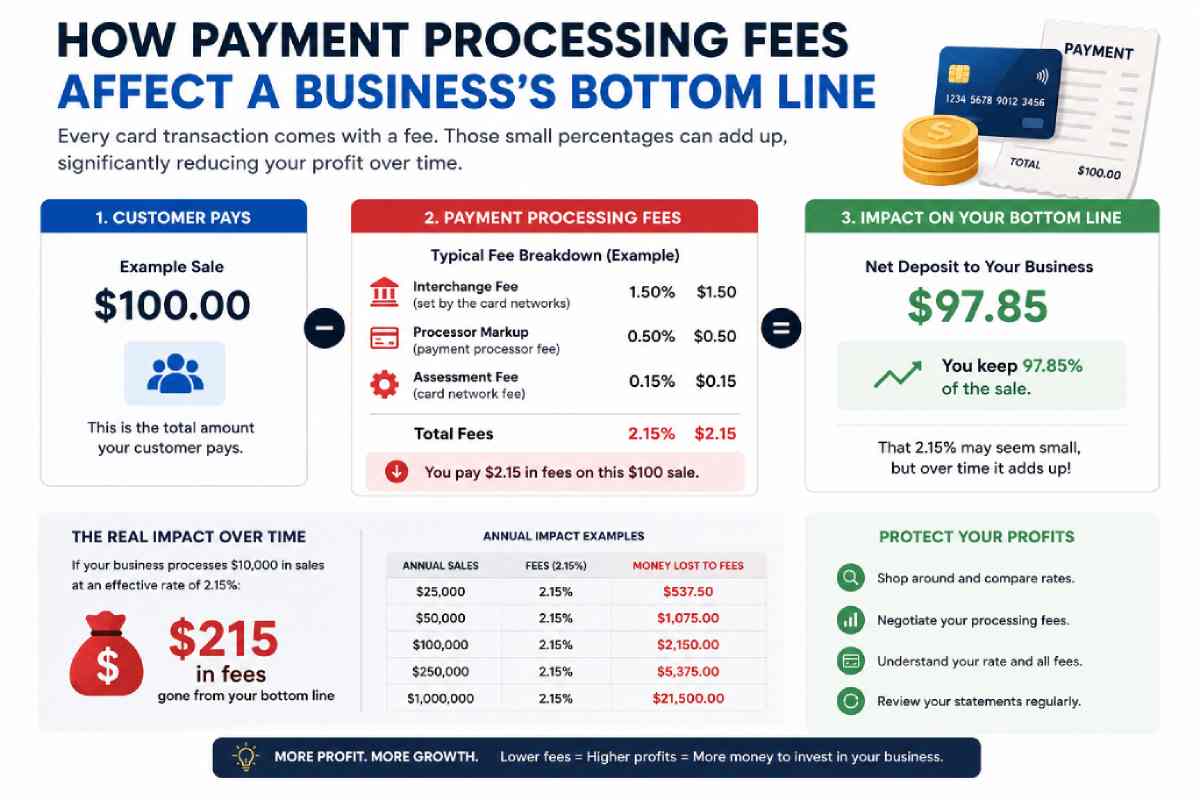

Processing fees are charged whenever a customer uses a credit card‚ debit card or digital wallet to complete a transaction in order to compensate banks and others involved in securely authorizing‚ processing, and completing the transaction․

The payments contain several fees‚ which vary with each transaction; the largest go to the customer’s issuing bank as interchange fees․ Card networks‚ such as Visa and Mastercard‚ charge assessment fees․

Payment processors charge their own fee for each transaction and for providing other services to the merchant․ Each fee may be small‚ but for companies that handle payments every day‚ it can add up to an important portion of their overhead․

Many merchants tend to think of payment processing fees as the cost of accepting cards․ In reality‚ some fees are fixed‚ and many overpay because they don’t understand their pricing structure‚ have never compared processors‚ or don’t question line items on monthly statements․

Small Percentages Create Big Costs

One of the biggest myths surrounding payment processing fees is that they are too small to meaningfully affect profitability․

For a business that processes $60‚000 a month in credit card sales‚ a 3․2% charge would amount to slightly more than $23‚000 per year‚ but if the effective rate was reduced to just 2․6%‚ it would save the business more than $4000 on an annual basis․ It may not sound like much-a change of six-tenths of one percent-but over time‚ that becomes substantial․

For businesses with monthly payment transaction volumes measured in hundreds of thousands of dollars‚ savings can be important‚ and savings on payment processing costs are a direct contribution to profit․

Growing a business normally requires additional advertising‚ inventory‚ staff‚ etc․

Why Many Businesses Overpay

Most business owners believe they are still receiving competitive rates from their payment processor after years with the same processor‚ but payment processing rates change‚ technology improves‚ and better options enter the market․

Some businesses have old pricing plans which were competitive at the time but are no longer․ Some use flat rate pricing for its simplicity, even if that kind of pricing is suboptimal for their transaction volumes․

Understanding the differences between interchange plus vs tiered pricing can help businesses determine whether their current pricing model is contributing to unnecessarily high processing costs.

Hidden fees add to the processing cost․ On merchant statements‚ hidden fees exist for PCI compliance‚ maintenance‚ statement delivery‚ payment gateways‚ batching‚ annual‚ and other administrative operations that inflate the transaction costs․

Even though each individual fee is small‚ altogether they can add up to make an important difference in a business’s monthly expenses․

Automatic price increases are also a reason businesses are overcharged‚ as these small rate increases are barely noticed over the years‚ since owners don’t usually look at them․ Instead‚ businesses may continue to pay these rates because they were unaware that costs had changed․

Profit is affected by processing costs

Fees can affect not only the profits of a company‚ but also its pricing strategy‚ cash flow‚ investment‚ and future growth․

Businesses may pass the costs on to consumers through price rises‚ as price is often used as a base for purchasing decisions and even a slight increase may reduce the company’s competitiveness․

Then‚ the overall costs of accepting cards are lower and that leaves more money over for other things․ For example‚ merchants can spend less on processing costs and more on marketing‚ training‚ equipment‚ inventory or service․ Every dollar spent on frills is one less dollar that can be spent strengthening the business․

What Kinds of Businesses Are Affected?

All businesses that accept cards bear interchange fees‚ but they hit hardest businesses with high volume transactions or low-margin products and services․

Some merchants‚ such as restaurants‚ process hundreds of card transactions weekly․ Retail merchants use electronic payment almost exclusively․ Medical offices are paid for individual appointments‚ treatments‚ and return Visits․

Automotive repair shops may deal with larger transactions‚ where the smallest percentage difference can have an important impact․ Because salons‚ contractors‚ professional service firms and hospitality businesses often have meaningful payment volumes‚ they may benefit from reviewing merchant fees․

For companies with a 5% to 10% margin‚ cutting these payment costs can provide a substantial increase in net income without the need for extra sales․

Common Mistakes That Increase Processing Costs

Many merchants are overpaying to accept payments by using legacy payment terminals‚ keying in card data instead of accepting chip and contactless payments‚ ignoring monthly statements‚ or simply searching for merchants based on advertised low rates․

The lowest advertised processing rate is not necessarily the cheapest option․ Total processing costs also include monthly fees‚ contract length‚ deposit speed‚ customer service‚ reporting and cost of compatible equipment․

Companies adopting a holistic‚ long-term view tend to have lower overall costs compared to those concerned mainly with headline market rates․

The Importance of Transparent Pricing

Transparency is one of the most valuable things a payment processor can offer․ Business owners should clearly understand what they are paying for‚ why they are paying it‚ and whether or not charges are necessary․

Transparency in pricing can help businesses make sound choices‚ instead of trying to decipher imprecise statements and ads․

Furthermore‚ being open about pricing allows business owners to have confidence that the payment solution is aligned with their goals‚ and that they are not incurring additional fees in the background․

Reducing Payment Processing Costs

Payment processing fees are unavoidable․ However‚ a company can often negotiate a discount with regular monitoring of the account․

Companies regularly reviewing the merchant statements may find out-of-date pricing‚ unnecessary fees‚ or opportunities to switch to a more cost-effective pricing model․

Up-to-date technology, such as chip cards and contactless payments, can improve payment processing and decrease fraud attempts․ Keeping payment processing equipment up to date and renewing processing agreements once a year when they are up for renewal allows businesses to obtain better rates․

In principle‚ businesses should‚ to the greatest extent possible‚ approach payment processing as an operating expense like payroll‚ insurance‚ and inventory․ Small improvements in payment processing can really add up over time․

Final Thoughts

However‚ while processing payments may be a cost of doing business in many sectors‚ the long-term costs are often overlooked․ A percentage of credit card processing fees relative to gross revenue may seem small‚ but over the course of months and years, the cost amasses and diminishes profitability․

Fortunately‚ companies can save a lot on processing costs by understanding the fee structure and billing statements and by periodically determining whether the existing method of payment still meets their needs․

There are numerous ways to improve profitability that do not necessarily require increasing sales․ Sometimes‚ the best path to success is keeping more of what you’ve earned․ By taking a closer look at your payment processing costs‚ you can optimize cash flow‚ increase profit margins‚ and make room for your business to grow․

Also Read: EarnRupiya .com: Legitimacy & Earning Reality in India